{kind=link}

Indian household balance sheets exhibit a set of features that is unusual in the international context:

Indian household balance sheets exhibit a set of features that is unusual in the international context:

A disproportionately high share of wealth allocated to physical (i.e. non-financial) assets, such as gold.

Under-investment in long-term insurance and pension products.

A dis-proportionally large reliance on unsecured debt, mostly from non-institutional sources (e.g. moneylenders).

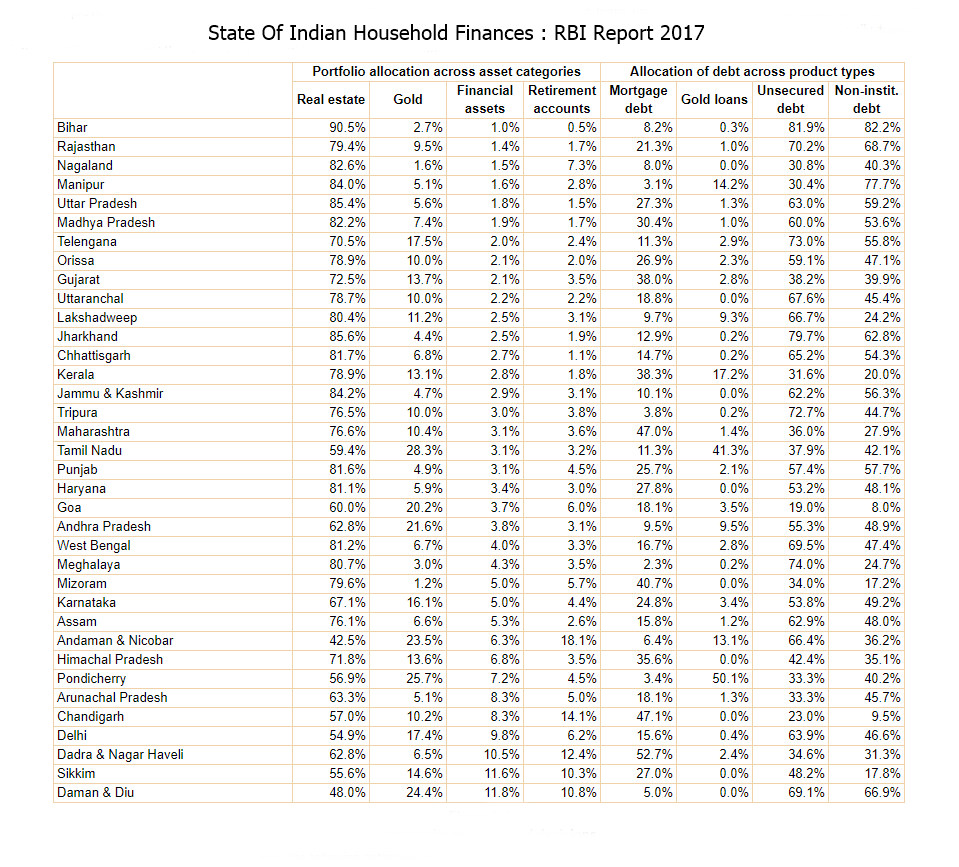

The recently submitted report of the committee on household finance shows that only 5% of the average Indian household’s wealth is in financial assets. The other 95% is in physical assets—77% in real estate, 7% in durables such as vehicles, livestock and equipment and 11% in gold.

The report also finds that financial assets account for a very low portion of the balance sheet of the rich. The survey does find that higher education is associated with a lower share of real estate, and higher shares of both pensions and financial wealth. The report is sceptical, pointing out that higher education is correlated with employment in the formal sector— with fewer opportunities for tax evasion, and more exposure to formal financial markets. In particular, says the report, richer households may find it easier to place illicit earnings or engage in tax evasion by investing in real estate, thereby avoiding the scrutiny associated with investments in the formal financial sector. The role of real estate as a swamp to cover up black money is behind the affection of the rich for investment in the sector.

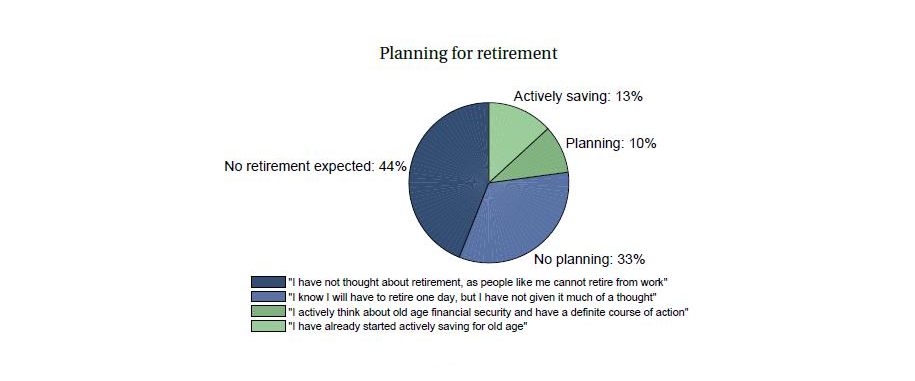

How does asset allocation play out over the life cycle of the average Indian household? The largest fraction of the wealth of young households in India is in the form of durable goods and gold. Why gold? Lack of trust in financial institutions is a big reason. As they approach retirement, more household wealth is held in land and housing, in marked contrast to the developed nations, where people have a nest egg of financial savings to fall back upon after retirement.

The report points out Indian households are exceptional, as India is the only country in which mortgages account for an increasing share of total liabilities as people approach retirement age, leaving them exposed to repayment risk even in old age. What’s more, over the coming decade and a half, the elderly cohort is expected to grow by 75% and the financing of health expenses and consumption during retirement is expected to leave older households particularly vulnerable to adverse shocks.

Strangely, the high share of real estate in household portfolios is not accompanied by an equivalent share of mortgages in total household debt. In fact, 56% of household debt is unsecured, reflecting high reliance on non-institutional sources such as moneylenders. Moreover, the major reasons for households getting into debt are loss of crops and livestock, medical emergencies, and the effects of natural disasters. Half the households count on help from family, friends and moneylenders to tide over these emergencies.

For medical expenses, 69% of households draw upon informal sources of funding, 26% of which are loans from moneylenders. This clearly points to the precarious financial situation of the majority of Indian households.

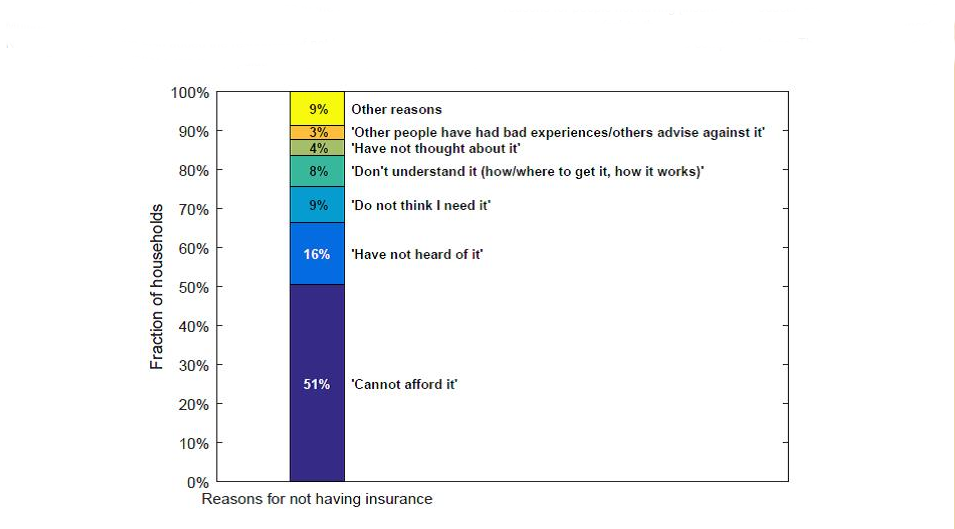

The main three risks that households face (i.e. the loss of crops and livestock, major medical emergencies, and damage to physical assets due to natural disasters) are all insurable. So why don’t households buy insurance? The report says the main reason is not lack of awareness, but affordability.

The committee points out that allocating a larger proportion of savings to financial instruments will raise returns for households and recommends a number of excellent measures for improving financial inclusion. The government’s crackdown on the real estate sector and on black money is already seeing a flood of money into the financial markets.

With modern technology, the costs of financial inclusion have fallen dramatically, enabling a reaching out to the poor. The fact remains, though, that there must be adequate income in the first place before people can save and allocate savings to financial assets.

Here are some facts the report brings out: only 65% of Indian households in which the household head is younger than 35 years of age hold any financial assets; only 55% of the poorest households hold any financial assets; only a quarter of households are able to deal with emergency expenses by drawing upon accumulated wealth; very low-income households wish to save nearly 65% of their annual income in an effort to repay past loans.

All these facts reflect the very low levels of income and savings for most households in India.

The largest fraction of the wealth of young households in India is in the form of durable goods and gold. The largest share of wealth as Indian households approach retirement is held in land and housing.

Financial assets and pensions account for a very low portion of the total balance sheet even for the rich.

Unsecured debt accounts for two-thirds of total liabilities for the very poor, and one-third for the rich.