{kind=link}

Interest in global stocks, especially tech stocks listed on US stock exchanges, have captured the attention of investors around the world. Whether you are an experienced investor or have just started out, you have to comply with certain tax rules when you invest outside India. For one, when you sell your foreign investments, the gains are taxed at different rates than the gains from domestic investments. Here are some things to keep in mind.

Gains are tax free abroad…

The first thing to note is that foreign residents are exempted from capital gains tax in most countries, including the US and UK. Whether you make short-term or longterm gains on stocks and mutual funds, you don’t have to pay tax. Dividends and interest earned are also tax free. However, rental income and gains made from sale of property and real estate linked instruments are taxable.

… but are taxable in India

If a stock or mutual fund listed on foreign exchanges is held for more than two years, the gains from the sale are treated as longterm capital gains. These long-term gains are taxed at 20% after indexation of cost. The exemption of ₹1 lakh per year, which is available on long-term capital gains on sale of shares and equity-oriented mutual funds in India, is not available on foreign stocks.

When foreign stocks are held for two years or less, the gains are treated as short-term gains. The amount gets added to the income of the investor and is taxed at the applicable slab rate. Gains made on employee stock options (ESOPs) and restricted stock units (RSUs) in foreign companies are also taxed in the same manner.

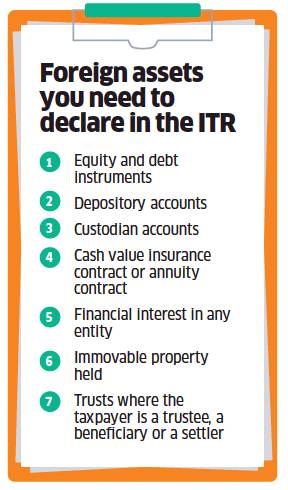

Disclosing foreign assets in tax return

The most important thing to note is that if you are a tax resident of India, you are required to disclose all foreign assets and foreign income in your income tax return. Even if there is no income, the assets must be declared in the return. This reporting is required for assets held at any time during the year. Even if you have sold the asset and don’t own it as on 31 March of the financial year, you still have to declare the information about the asset (and any income earned from it) in your tax return. Also note that filing of income tax return is mandatory for those who own foreign assets even if their total income from all sources is below the minimum exemption limit of ₹2.5 lakh. These include assets that may have been held by you as a beneficial owner. Taxpayers who have foreign assets cannot file their return using ITR-1. The details can only be reported in ITR-2 or ITR-3, as applicable.

Tax on global funds varies

Certain mutual funds have exposure to foreign stocks. The tax on the gains from such funds depends on the exposure these funds have to Indian stocks. If the exposure to Indian stocks is more than 65%, then the gains will be taxed in the same manner as equity oriented funds. If held for more than 12 months, the gains will be treated as long-term capital gains with an exemption of ₹1 lakh per year. Gains above ₹1 lakh will be taxed at 10%. If held for one year or less, the gains will be treated as short-term gains and taxed at 15%.

If a fund has less than 65% invested in Indian stocks, it will be treated like a non-equity fund. If held for more than three years, the gains will be classified as long-term capital gains and will be taxed at 20% with indexation. If held for three years or less, they will be treated as short-term capital gains. The amount will be added to the income of the investor and taxed at the normal slab rate.

Avoiding double taxation

In some cases, gains from sale of investments held outside India may get taxed in the foreign country. Gains are usually taxable if the investor is a tax resident in a country. If tax has been paid in a foreign country, you can claim credit for it in India if there is a Double Tax Avoidance Agreement (DTAA) between India and that country. India has entered into DTAAs with more than 150 countries, including the US, UK and most European countries.

While claiming tax credit, make sure you are referring to the correct DTAA. You will need to obtain a Tax Residency Certificate (TRC) that helps identify and certify the tax status to make sure the correct DTAA has been applied. Under DTAA, there are two methods to claim tax relief – exemption method and tax credit method. Under the exemption method, income is taxed in one country and exempted in another. In the tax credit method, where the income is taxed in both countries, tax relief can be claimed in the country of residence.

TCS is payable when you transfer funds

Under the Liberalized Remittance Scheme, a resident Indian can transfer up to $2.5 lakh (approximately ₹1.84 crore) abroad in a financial year. But there is a tax collected at source (TCS) if the amount exceeds ₹7 lakh in a year. The TCS is 5% of the amount exceeding ₹7 lakh, and can be claimed as a refund when the taxpayer files his income tax return.