{kind=link}

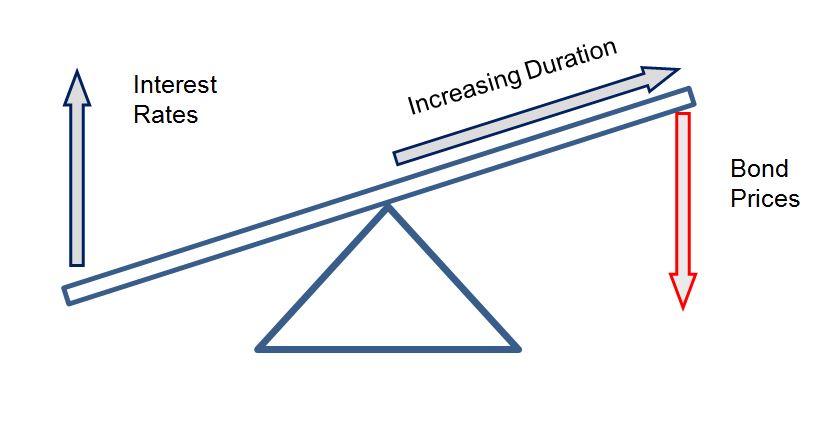

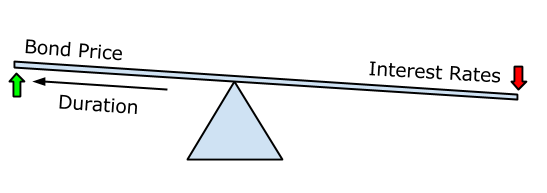

Duration is a measure of the interest rate sensitivity of a bond.

Bonds have two main risks associated with them: credit risk and interest rate risk.Duration addresses the interest rate risk of a bond.

Duration is a single measure of cash flow, tenor and yield of a bond. The periodic coupon payments shorten the average tenor of the bond.

Duration is measured in years. A high duration indicates that investors would need to wait for a long period to receive the coupon payments and principal invested.

Duration is also an alternate measure of the maturity of a bond.