{kind=link}

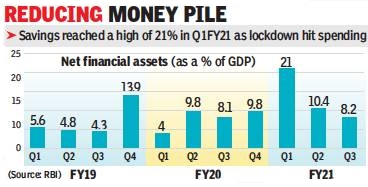

Indians saw their savings shrink and bank debt burden rise in the third quarter of the FY21 as the country emerged from the impact of the first wave of the pandemic and economic activity picked up. According to data released by the Reserve Bank of India, household savings fell to 8.2% of GDP in the quarter ended December 2020, down from 10.4% in the preceding quarter. Savings-to-GDP ratio had spiked to a high of 21% in the first quarter of FY21 as Indians held back from spending during the lockdown.

According to the RBI, the trend in deposits exhibits a sequential moderation for the second consecutive quarter driven by weaker flows into household financial assets, which more than offset the moderation in the flow of household financial liabilities. Financial assets as a share of GDP have fallen to 12.7% in the third quarter from 15.8% in the second quarter. The drop was seen across financial instruments. The pandemic has hurt households hard as they struggle to deal with the impact of the pandemic on jobs, income and spending.

The ratio of household (bank) deposits to GDP declined to 3% in Q3FY21 from 7.7%. Savings in life insurance and provident & pension funds as a share of GDP fell to 2.9% and 2.2% respectively in the third quarter from 3% and 2.6% in the preceding quarter.

Households moved their money from banks and held it in cash, resulting in household currency holdings as a percentage of GDP rising to 1.7% in the third quarter from 0.4% in the second quarter. Also, falling interest rates and the surge in stock valuations resulted in household investment in mutual funds rising from 0.3% of GDP at the end of September 2020 to 1.2% at the end of December.

SBI Group’s chief economist Soumya Kanti Ghosh said in a note that there was scope for an increase in household investments in equity from present levels. “Increasing retail participation, if it becomes the norm, could also enable a larger resource pool for financing India’s infrastructural requirements. For example, the share of savings in stocks and debentures to total household financial savings at 3.4% in FY20 is likely to increase in FY21 to 4.8-5%,” he said. This is still much lower than 36.5% in the US.

At the same time, liabilities of households from commercial banks rose to 27% of GDP, up from 26.3%. Despite higher borrowings from banks and housing finance companies, the flow in household financial liabilities was marginally lower in Q3FY21 following a marked decline in borrowings from non-banking financial companies.

The household debt-to-GDP ratio, which is based on select financial instruments, has been increasing steadily since end-March 2019. It rose sharply to 37.9% at the end-December 2020 from 37.1% at end-September 2020.