{kind=link}

Mr. Goregaonkar has sold his ancestral house for Rs.20 lakh. He has booked a new apartment which is due for possession within the two years. He is in a dilemma as the amount he has received is a capital gain in his hands and is liable to tax. His intention is to use this fund towards paying for his new house.

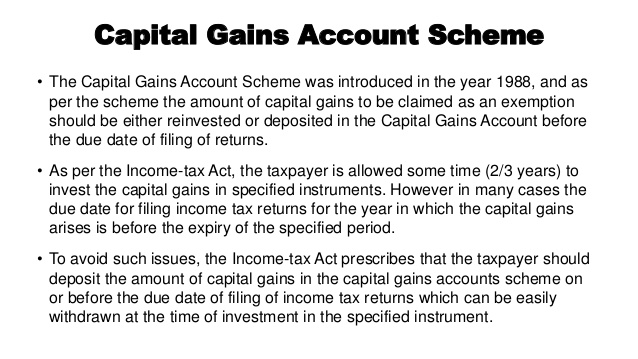

Capital Gains Account Scheme

As per the capital gains account scheme, Mr. Goregaonkary can keep the funds outside the ambit of taxation if he opens this account within the last date of filing his income tax returns and parks these funds there. As per the provisions of the IT Act he can save tax on long term capital gains provided:

*A residential property is purchased within two years of effecting the sale.

*A residential property is constructed within three years of effecting the sale.

How to open CGAS?

There are 28 state-owned banks where this account can be opened. Only urban and metro branches are permitted to offer this account and rural branches are not included.

Capital Gains Account – Type A – Savings Account: This is like a normal savings account and the interest payable on this account is the same as the rate of interest paid on any normal savings account by that particular bank.

Capital Gains Account -Type B – Term Deposit Account: This resembles a fixed deposit account, wherein the amount is deposited for a fixed period of time. The interest rate on this account is equivalent to the interest paid on fixed deposits by the bank. As Type B accounts are same as fixed deposits account, any withdrawal from this type of account attracts a penalty for pre-maturity withdrawal.

Interest earned from both the accounts is liable to be taxed and attract TDS.

If Mr. Goregaonkar has to make the final payment for his apartment at one go then he would be better served by opening the Type B account. For those who are constructing a house, Type A account would be a better option as this would provide the flexibility of multiple withdrawals.

Withdrawing funds from CGAS

The amount deposited in the CGAS can be withdrawn by making an application in the appropriate form. The amount so withdrawn needs to be utilised within 60 days from the date of such withdrawal and only for the specific purpose for which such withdrawal was made. The unutilised amount has to be re-deposited immediately. For subsequent withdrawal, an application has to be made mentioning details of the purpose in which the previous withdrawal was utilised. Most banks do not issue any cheque books to the CGAS holders as the withdrawal is effected by filling up the specified form only. Any amount over Rs.25,000 is disbursed by the bank through demand drafts directly in the name of the vendor or builder.

Closing the account

The income tax assessing officer can approve the closure of the account. On the closure of the account or after the lapse of three years, whichever is earlier, the entire unutilised funds lying in the account are liable to be taxed under capital gains. Only individuals and HUF are permitted to open the account and the amount deposited is inadmissible as security for any loan or guarantee. The taxpayer can also appoint nominees to this account by making an application in the appropriate form.