{kind=link}

Interim Finance Minister Piyush Goyal has proposed a few key changes to cheer the low-income and middle-income group individual taxpayers.

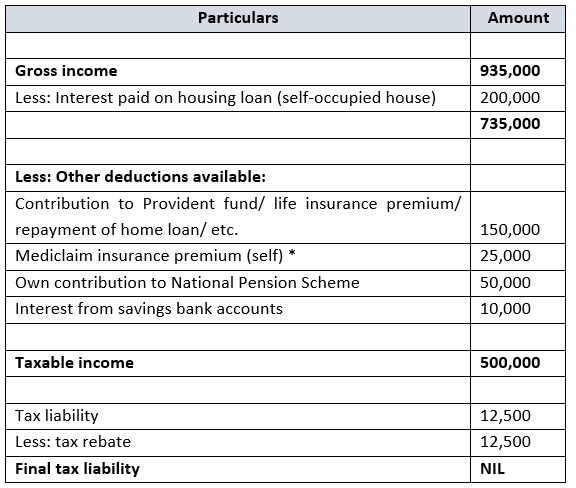

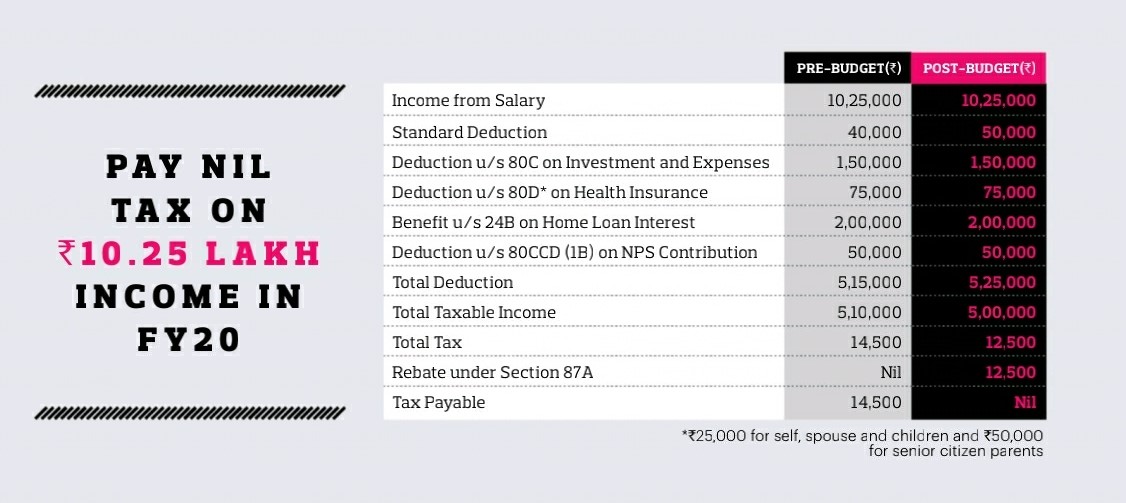

The most important proposal of the budget is the increase in the income tax rebate limit from Rs.2,500 (on taxable income upto Rs.350,000) to Rs.12,500 (on taxable income of upto Rs.500,000). Beyond the exemption limit of Rs.250,000, tax currently applies at 5% upto taxable income of Rs.500,000. As can be seen, the budget proposal effectively means that the entire tax liability is nullified for someone who is earning taxable income of upto Rs.500,000. The budget speech also outlined the fact that this NIL-tax income level is actually much higher, if the deductions (e.g., for tax saving investments/ eligible expenses, etc.) are taken into account –

* Additional Rs.30,000 deduction available if premium paid for parents (higher deduction for senior citizens).

However, it is very important to note that such taxpayers will still be required to file their annual tax returns within the prescribed timelines and the proposed change is in the tax rebate and not in the tax slabs or tax rates. Therefore, this proposal will not benefit individuals having taxable income more than Rs.5 lakh.

Another important change proposed is increase in the limit of the standard deduction available to salaried taxpayers from Rs.40,000 to Rs.50,000. Unlike the tax rebate change, which applied only to taxpayers with smaller income, this is a universal change for salaried class, providing benefit to all employees. As this directly reduces the taxable salary income by an additional amount of Rs.10,000, the tax liability also reduces as per the applicable tax rate. For example, for an individual having taxable income of less than Rs.10,00,000 (highest applicable tax rate being 20%), this results in tax savings of Rs.2,080 (including 4% cess). Similarly, for someone earning taxable income of over Rs.1,00,00,000, the savings will be Rs.3,588 (including impact of 15% surcharge and 4% cess).

Another proposed change relates to exemption from notional rent taxation in respect of a second house property. Currently, if a person has two properties that are either self-occupied or unoccupied due to employment/ business in another place, the taxpayer needs to pay income tax by deeming one of these properties as if the same is fully rented out, resulting in notional income getting taxed. While this notional rental income taxation is not completely done away with, the same is proposed to be applied only from the third property onwards. This is expected to bring relief to a significant number of taxpayers who move from their hometown to take up employment in other towns/ cities and end up having to own/ maintain two houses.

Another interesting change proposed relates to extending the exemption for long term capital gains from sale of one house property to buy two house properties. For example, this will benefit in a situation where a family is split between, say, two sons, where the parent may need to sell the present single house and buy two houses for future needs. Presently, the long term capital gains exemption would be limited only to the investment in one of the two new properties. However, once the proposed change is enacted, the entire investment in both new properties will be eligible for calculating the exemption income. It is proposed that this exemption will be allowed only once in the lifetime of the taxpayer, and the maximum exemption will be limited to Rs.2 crore. As the provision for rollover of long term capital gains from one house property into another (single) house property remains unchanged, that benefit continues to be available in the future also.

It is also proposed to increase the threshold for deduction of tax at source on interest on fixed deposits with bank/ post office from Rs.10,000 to Rs.40,000. Assuming an interest rate of 8% per annum on a fixed deposit, this means that the banks will not be required to deduct interest income on a fixed deposit of Rs.500,000. This will also avoid the need for such small deposit holders who have no tax liability to submit Form 15G to banks so as to not be subject to TDS on their interest income.