{kind=link}

Reverse mortgage works well for families where kids are well settled and don’t need the parents’ house.

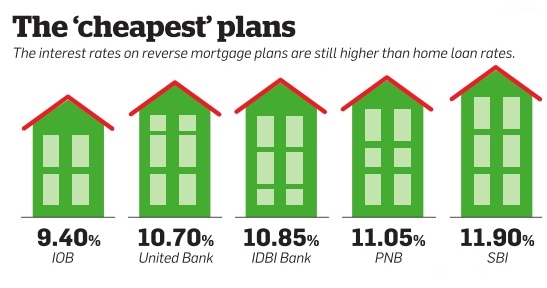

Reverse mortgage can be of two types: Either the bank can pay you money at regular intervals–monthly, quarterly or annually–or, it can pay you a lump sum, which you can use to buy a pension plan from life insurance companies. Experts recommend that it is better to avoid the second option. Pension from insurance companies is fixed forever, while banks usually review the annuity amount every five years and there is a probability of the annuity going up after five years. Also, regular payouts received from banks are treated as loans and, therefore, will be tax-free in your hands. Pension from life insurance companies, however, is treated as income and you will have to pay tax at marginal rates.

Only citizens aged 60 or more are eligible. For married couples, jointly taking the loan, one of them should be above 60. Some banks may have additional conditions –joint applicant to be above 55, etc. Reverse mortgage is allowed only against self-occupied residential property. The title of the property should be clear–there should not be legal, ownership issues with the property. The tenure for which the loan is granted varies across banks, but the maximum period for which is its allowed is 20 years. The loan tenure usually is the same as the residual life of the property. Banks can recover the loan only on the death of both the borrowers. For example, the loan tenure is 20 years and the borrowers live for 25 years, the lender can only recover the loan after 25 years. The heirs have the right to settle the loan–principal and interest. If they decide not to settle it, the house is sold and any proceeds in excess of the sum due to the bank, is returned to the legal heirs. The documentation is similar to that of a housing loan. Just like other loans, the processing fee needs to be borne by the borrower. The borrower also has to cover all the home insurance premiums.