{kind=link}

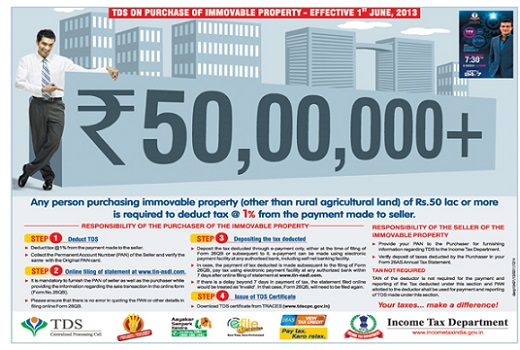

Since June 2013, it has been mandatory for buyers of immovable property to deduct TDS from the amount to be paid to the seller. It is the responsibility of the buyer to deduct TDS if the transaction value exceeds Rs.50 lakhs. The buyer is required to deduct TDS @ 1% on the total consideration and deposit the same in the account of the income tax authorities in the prescribed format.

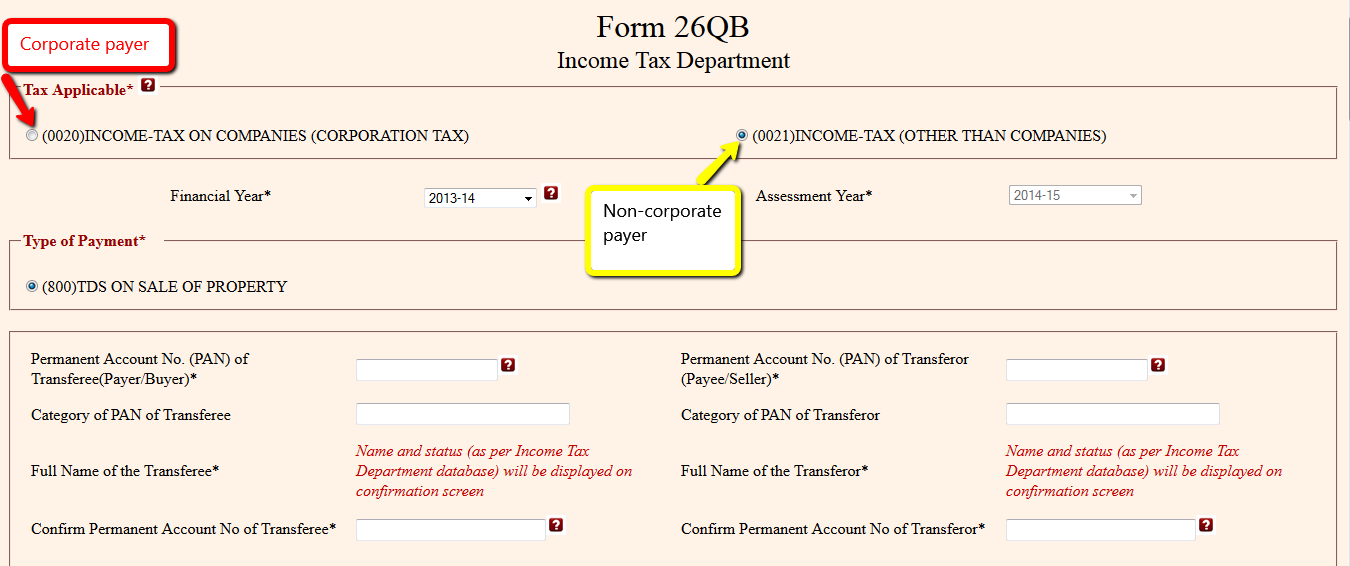

Form 26QB must be filled by the buyer either online or offline to deposit the TDS.

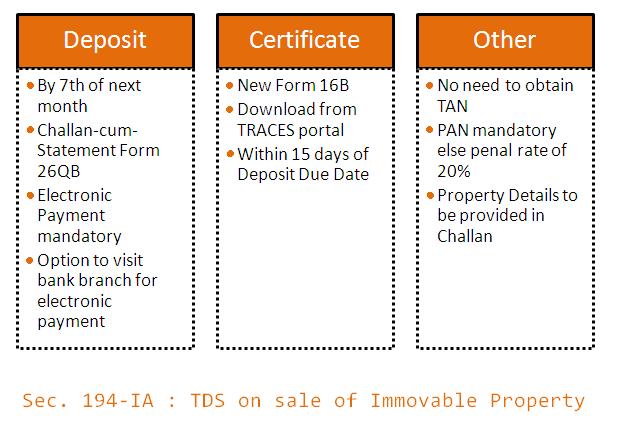

The challan (Form 26QB) must be filed within 7 days from the month in which the TDS was deducted by the buyer.

Information with respect to the buyer and seller (name, address, PAN, status), details of the property, consideration and TDS payable must be entered in the form.

One can choose to pay either through Netbanking or at the branch of the bank. If the taxpayer chooses e-tax payment on subsequent date at the bank branch, an acknowledgement number is generated. This number must be retained by the taxpayer to be presented to the bank while making the payment.

Once the form is filed and payment made to the income tax authorities, approved form 26QB or form 16B can be downloaded by logging into TRACES as a tax payer.Form 16B must be provided by the buyer to the seller as a proof of deposit of TDS.

Dealings in agricultural land are excluded from the requirements of these provisions.

If the consideration is being paid in installments, TDS must also be deducted on each installment.

If PAN is not provided by the seller, TDS @ 20% is deductible.